At WT Wealth Management we have always understood the “drag” fees and expenses could potentially have on your portfolio. Lower cost is a fundamental reason why we primarily use ETF’s when we build client portfolios. ETF’s generally have much lower expense ratios than mutual funds. ETF’s replicate an index, there is no highly compensated manager at the helm making buy and sell decisions. Mutual funds are paid to beat an index. Unfortunately, in most cases they fail to do so. Over the last few years active managers have under performed their respective Index/Benchmark at a shocking rate of nearly 88%. That’s right!! Nearly 9 out of 10 active managers fail to deliver a rate of return even equal to their stated benchmark. Investment advisors that use mutual funds are hitting their clients with the preverbal “double whammy”; under performance and a more costly product.

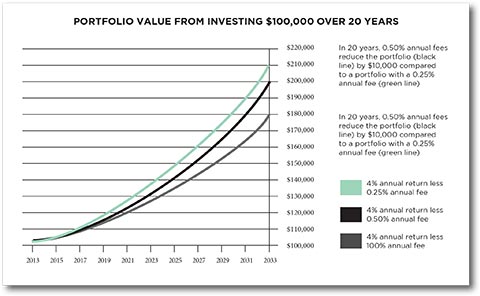

The following chart shows an investment portfolio with a 4% annual return over 20 years when the investment either has an ongoing fee of 0.25%, 0.50% or 1%. Notice how the fees affect the investment portfolio over 20 years

When choosing either a financial professional or a particular investment, be sure you understand and compare

the fees you could potentially be charged. This is important and could save you a lot of money in the long run.

At WT Wealth Management, we routinely lower clients’ fees as they consolidate additional assets into our

firm. We’ve built our organization with a daily focus on putting the client’s interest ahead of our own, by

searching out lower cost investment vehicles compounded with keeping our fees in line with the lowest cost

investment managers in the industry. Portfolio returns can be out of our control. The expenses in your portfolio is something we can control & impact.

In the below section, we thought about some questions you should ask yourself and any investment advisor

you are working with or considering working with.

How do I know what I’m being charged?

Find out what you may be charged by reading what your financial professional provides you. Get informed,

look at your account application documents, account statements, confirmations and any product-specific

documents to see the types and amount of fees you are paying. Fees impact your investment returns, so it’s

important you understand them. Every investor should thoroughly read anything that they sign, especially the advisors Investment Management Agreement (IMA).

Ask questions so that you understand what you will be charged, when and why.

Questions might include:

What are all the fees relating to this account?

Do you have a fee schedule that lists all of the fees that will be charged for investments and maintenance of

this account?

What fees will I pay to purchase, hold and sell this investment?

Will those fees appear clearly on my account statement or my confirmation? If those fees don’t appear on my

account statement or my confirmation, how will I know about them?

How can I reduce or eliminate some of the fees I’ll pay?

Can I pay lower fees if I open a different type of account? Do my fees go down if I add more money to my

accounts?

Do I need to keep a minimum account balance to avoid certain fees?

Are there any other transaction or advisory fees? Account transfer, account inactivity, wire transfer fees or

any other fees?

How do the fees and expenses of the product compare to other products that can help me meet my

objectives?

How much does the investment have to increase in value before I break even?

Ask questions about your financial professional’s compensation.

Questions might include:

How do you get paid?

By commission? How are commissions determined? Do they vary depending on the amount of assets you

manage?

Do you get paid through means other than through commissions and amount of assets you manage and,

if yes, how?

Do I have any choice on how to pay you?

Check your statements. Review confirmation and account statements, to be sure you’re being charged correctly

and ask your financial professional to break the fees down for you if it’s unclear.

What types of fees are there?

Fees typically come in two types—transaction fees and ongoing fees. Transaction fees are charged each time

you enter into a transaction, for example; when you buy a stock or mutual fund. In contrast, ongoing fees or

expenses, are charges you incur regularly, such as an annual account maintenance fee.

How do transaction fees affect your investment portfolio?

Transaction fees are charged at the time you buy, sell or exchange an investment. As with any fee, transaction

fees will reduce the overall amount of your investment portfolio.

How do ongoing fees affect your investment portfolio?

Ongoing fees can also reduce the value of your investment portfolio. This is particularly true over time,

because not only is your investment balance reduced by the fee, but you also lose any return you would have

earned on that fee. Over time, even ongoing fees that are small can have a big impact on your investment

portfolio. Review chart above.

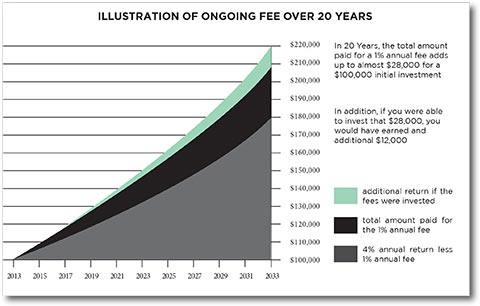

The chart below illustrates the impact of a 1% ongoing fee on a $100,000 investment portfolio that grows 4%

annually over 20 years. As the investment portfolio grows over time, so does the total amount of fees you

pay. Because of the fees you pay, you have a smaller amount invested that is earning a return. A manager that

charges 1.5% needs to generate a higher return than a manager that charges 1%.

Commissions. You will likely pay a commission when you buy or sell a stock through a financial professional.

The commission compensates the financial professional and his or her firm when it is acting as agent for you

in your securities transaction.

Markups. When a broker-dealer sells you securities out of its inventory, the broker-dealer acts as a principal in

the transaction (that is, selling to you directly the securities it holds). When acting in a principal capacity, the

broker-dealer generally will be compensated by selling the security to you at a price that is higher than the

market price (the difference is called a markup), or by buying the security from you at a price that is lower than

the market price (the difference is called a markdown).

Sales loads. Some mutual funds charge a fee called a sales load. Sales loads serve a similar purpose to

commissions by compensating the financial professional for selling the mutual fund to you. Sales loads can be

front-end, in that they are assessed at the time you make your investment or back-end in that you are assessed

the charge if you sell the mutual fund usually within a specified time frame.

Surrender charges. Early withdrawal from a variable annuity investment (typically within six to eight years,

but sometimes as long as 10 years) will usually result in a surrender charge. This charge compensates your

financial professional for selling the variable annuity to you. Generally, the surrender charge is a percentage of

the amount withdrawn, and declines gradually over a period of several years.

Investment advisory fees.

If you use an investment adviser to manage your investment portfolio, your adviser will charge you an ongoing

annual fee based on the value of your portfolio.

Annual operating expenses.

Mutual funds and exchange-traded funds, or ETFs, are essentially, investment products created and managed

by investment professionals. The management and marketing of these investment products result in expenses

and costs that are often passed on to you—the investor—in the form of fees deducted from the fund’s assets.

These annual ongoing fees can include management fees, 12b-1 or distribution (and/or service) fees, and

other expenses. These fees are often identified as a percentage of the fund’s assets—the fund’s expense ratio

(identified in the fund’s prospectus as the total annual fund operating expenses).

Account Maintenance Fees.

The expenses for operating and administering your custodial account, brokerage account or IRA account

will be passed along to investors. This is in addition to the annual operating expenses of the mutual fund

investments that you may hold in your account.

Annual variable annuity fees.

If you invest in a variable annuity, you may be charged fees to cover the expenses of administering the variable

annuity. You also, may pay fees such as insurance fees and fees for optional features (often called riders).

You will also be subject to the annual operating expenses of any mutual funds or other investments that the

variable annuity holds.

What are some examples of products with combined transaction and ongoing fees?

Some investment products or services, including mutual funds, ETFs and variable annuities, commonly include

both transaction and ongoing fees as part of the structure of the product or service. For example, an ETF

is bought and sold like stock, so you may be charged a commission when you use a financial professional

to purchase an ETF. An ETF also typically has ongoing fees in the form of its expense ratio, referred to in

the ETF’s prospectus as the total annual fund operating expenses. You can use FINRA’s Fund Analyzer to

compare the cost of various types of securities, including mutual funds and ETFs.

What other fees might I pay?

In addition to commissions, a broker-dealer may also charge certain additional fees such as fees for not

maintaining a minimum balance, account transfer fee, account closure fee, account inactivity fee, wire transfer

fee, alternative investment fee or other fees. These fees may not always be obvious to you from your account

statement or confirmation statement. You should obtain information about all the fees you are charged and

why they are charged. Ask your investment advisor to explain the fees if you do not understand them.

What can I do if I think my fees are too high?

Follow up.

If your fees seem too high, ask questions. Consider following up in writing if you are not satisfied.

Negotiate.

In some cases, fees are negotiable, so you can talk to your financial professional about reducing them.

Shop around.

Just like shopping around for the best price on any other product or service, you should consider how much

you are paying for investing services. However, to the extent you decide to move to a new firm, you should

think about any tax consequences and fees for closing or transferring your account, for example, if you have

to sell some or all of your current holdings in order to transfer.

At WT Wealth Management we always do what’s in our clients best interest. This ranges from delivering the some of the

lowest Investment Management fees in the industry to constantly reviewing the ETFs and Mutual Funds we

use for hidden expenses while constantly seeking out lower cost alternatives. In many cases the ETFs we use

are on the TD Ameritrade “commission free” list just adding to and complementing our low cost approach. We

would never use something just because it’s cheaper, but in many cases like a S&P 500 Index Fund the lowest

cost option is usually the best option.

We are not in this business for us, we are in it for you. We know that if we do our jobs you’ll refer friends, family

and spread the good word about WT Wealth Management. We are always honest, upfront and transparent

about your account and what we charge.

If at any time you have a question. Please contact us.

WT Wealth Management is a manager of Separately Managed Accounts (SMA). Past performance is no indication of future performance. With SMA’s, performance can vary widely from investor to investor as each portfolio is individually constructed and allocation weightings are determined based on economic and market conditions the day the funds are invested. In a SMA you own individual ETFs and as managers we have the freedom and flexibility to tailor the portfolio to address your personal risk tolerance and investment objectives ñ thus making your account “separate” and distinct from all others we potentially managed.

An investment in the strategy is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Any opinions expressed are the opinions of WT Wealth Management and its associates only. Information is neither an offer to buy or sell securities nor should it be interpreted as personal financial advice. You should always seek out the advice of a qualified investment professional before deciding to invest. Investing in stocks, bonds, mutual funds and ETFs carry certain specific risks and part or all of your account value can be lost.

In addition to the normal risks associated with investing, narrowly focused investments, investments in smaller companies, sector ETF’s and investments in single countries typically exhibit higher volatility. International, Emerging Market and Frontier Market ETFs investments may involve risk of capital loss from unfavorable fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political instability that other nation’s experience. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Bonds, bond funds and bond ETFs will decrease in value as interest rates rise. A portion of a municipal bond fund’s income may be subject to federal or state income taxes or the alternative minimum tax. Capital gains (short and long-term), if any, are subject to capital gains tax.

Diversification and asset allocation may not protect against market risk or a loss in your investment.

At WT Wealth Management we strongly suggest having a personal financial plan in place before making any investment decisions including understanding your personal risk tolerance and having clearly outlined investment objectives.

WT Wealth Management is a registered investment adviser located in Jackson, WY. WT Wealth Management may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any subsequent, direct communication by WT Wealth Management with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of WT Wealth Management, please contact the state securities regulators for those states in which WT Wealth Management maintains a registration filing.

A copy of WT Wealth Management’s current written disclosure statement discussing WT Wealth Management’s business operations, services, and fees is available at the SEC’s investment adviser public information website ñ www.adviserinfo.sec.gov or from WT Wealth Management upon written request. WT Wealth Management does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to WT Wealth Management’s web site or incorporated herein, and takes no responsibility therefor. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Reach us directly at 800-825-0616

or by using the contact form below.