I am often asked:

“What are the current risks in this market?”

“How high will the markets go?”

“Are we in for a sell-off?”.

At WT Wealth Management, we have taken the time to review and analyze what we believe are the most likely

risks to the current bull market, which has entered its seventh year. Risks to the world economies remain modestly

to the downside, and drivers include weak global growth and a sudden change to expectations regarding

the U.S. Federal Reserve’s

interest rate path.

In several quarterly economic

outlooks we have reviewed,

many experts speculate

a 20-30% chance of an

economic “hard landing” for

China, though it is the world’s

second-largest economy. The

potential for policy errors in

China are real—and all the

more so, since a new bubble

appears to be building in the

property market. We at WT

Wealth Management have

favored more developed

countries such as Japan and

the European continent over

China and emerging markets, regarding our international

equity allocations.

Most economists have China’s GDP pegged at 6.5% this year. A sharper-than-expected deceleration in the

Chinese economy could reverberate around the world. We term risks like these a “black swan” — a metaphor for

surprise events that severely affect the global economy.

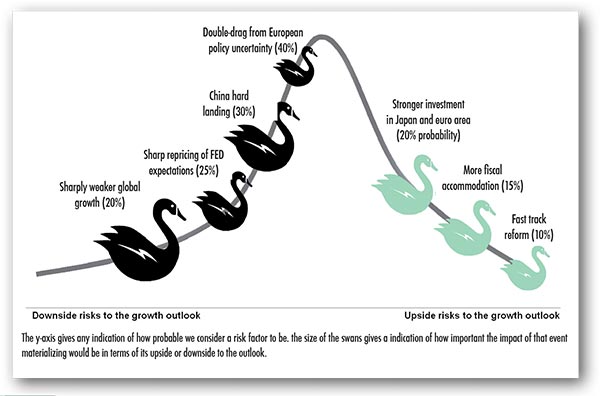

In our view, here are the top economic risks (black swans) to global growth, and their respective probabilities:

Uncertainty about Europe’s political direction is another risk to the world economy. The near-election of

a far-right president in Austria this month, coupled with the U.K.’s upcoming referendum on leaving the

European Union, have brought regional politics into sharper focus. Many economists forecast a 40% risk that

an unexpected political turn in Europe could double the drag from policy uncertainty on economic growth.

With a very busy political agenda lined up for the coming quarters, the risk of an event delivering an

unexpected outcome remains high, be it the OMT (outright monetary transactions) judgment from the German

Constitutional Court on June 21, the U.K. ‘Brexit’ referendum on June 23, the election of Spain’s 12 Cortes

Generales on June 26, the Italian constitutional referendum in October, and, heading into 2017, elections in

France, Germany, Netherlands, and possibly Italy. Furthermore, most economists see growth in the 19 Eurozone

countries averaging 1.6% so far this year—hardly a rip-roaring economy.

Another potential “black swan” for the U.S. economy could be a disorderly repricing of market expectations

of when the Fed will raise rates again. In our view, markets are mulling whether the Fed will raise rates in June

or July, but we believe the next hike will not occur until July, and possibly even December. Early forecasts have

the central bank raising rates by 25 percentage points three times in 2017, but insufficient economic data is

available to play that guessing game.

However, if the Fed sends too hawkish a message, the risk is that the repricing could turn disorderly. On the

flipside, too dovish a Fed could see bond markets unnerved by higher inflation readings and an ever-tighter

labor market.

Many see ongoing policy divergence between the Fed and other major central banks. The Bank of Japan

is expected to continue on its current policy path, and the European Central Bank is presumed to taper

quantitative easing between March and December 2017.

Most economics students believe that the most pressing risks of a global recession had eased in the last

several months, but that a sharp disappointment to global growth would still pose a major risk to most global

economies. A prolonged negative market response is the most likely mechanism, other than an outright

recession, to take a slowdown.

Global growth continues, but at a sluggish pace that leaves the world economy more exposed to risks, according

to the IMF’s (International Monetary Fund) latest World Economic Outlook (WEO). The WEO forecasts global

growth at 3.2% in 2016 and 3.5% in 2017—a downward revision of 0.2% and 0.1%, respectively, compared with

the January 2016 Update.

MODERATE RECOVERY IN ADVANCED ECONOMIES

The WEO projects that growth in developed economies will remain modest, at about 2%. The recovery is

hampered by weak demand and partly held down by unresolved crisis legacies, unfavorable demographics,

and low productivity growth.

In the United States, expected growth this year is at 2.4%, with a modest uptick in 2017. Domestic demand will

be supported by improving government finances and a stronger housing market that will help offset the drag

on net exports coming from a strong dollar and weaker manufacturing.

In the Eurozone area, low investment, high unemployment and weak balance sheets weigh on growth, which

will remain modest, at 1.5% this year and 1.6% next year.

In Japan, both growth and inflation are weaker than expected, reflecting in particular a sharp fall in private

consumption. Growth is projected to remain at 0.5% in 2016 before turning slightly negative, to –0.1% in 2017,

as the scheduled increase in the consumption tax rate takes effect.

EMERGING AND DEVELOPING ECONOMIES SLOWING FURTHER

While emerging markets and developing economies will still account for the lion’s share of world growth in

2016, growth prospects across countries remain uneven, and generally weaker, than they were over the past

two decades. The WEO projects their growth rate to increase only modestly—relative to 2015—to 4.1% this

year and 4.6% next year. This forecast reflects a variety of factors:

Slowing growth in oil exporters, with oil price declines and a still-weak outlook for non-oil commodity

exporters including Latin American nations.

- The modest slowdown in China, where growth continues to shift away from manufacturing and investment

to services and consumption.

- Deep recessions in Brazil and Russia and weak growth in some Latin American and Middle Eastern countries,

particularly those hit hard by the oil price decline, intensifying conflicts, and security risks.

- Diminished growth prospects in many African and low-income nations, due to the unfavorable global

environment.

On the positive side, India remains a bright spot, with strong growth and rising real incomes. The ASEAN-5

economies—Indonesia, Malaysia, Philippines, Thailand, and Vietnam—are also performing well. And Mexico,

Central America, and the Caribbean are beneficiaries of the U.S. recovery and, in most cases, lower oil prices.

RISKS ARE ON THE RISE

In today’s environment of weak growth, risks to the outlook are now more pronounced. These include:

- A return of financial turmoil, impairing confidence. For instance, an additional bout of exchange rate

depreciations in emerging market economies could further worsen corporate balance sheets, and a sharp

decline in capital inflows could force a rapid compression of domestic demand.

- A protracted period of low oil prices could further destabilize the outlook for oil-exporting countries.

- A sharper slowdown in China

than currently projected could

have strong international spillovers

through trade, commodity prices,

and confidence, leading to a more

generalized slowdown in the

global economy.

- Shocks of a noneconomic origin

related to geopolitical conflicts,

political discord, terrorism, refugee

flows and/or global epidemics

loom over some countries and

regions. If left unchecked, these

shocks could have significant

spillovers on global economic

activity.

On the upside, the recent oil price decline may boost demand in oil-importing countries more than

currently envisaged, spurred by possible consumer perception that prices will remain lower for longer.

RAISING GROWTH STILL A PRIORITY

More aggressive policy actions to lift supply-and-demand potential could foster stronger growth in both

the short and longer term. The WEO emphasizes a three-pronged approach of mutually reinforcing policy

levers: (1) structural reforms; (2) fiscal support, with growth-friendly composition of revenue and spending,

and fiscal stimulus where needed and where fiscal space allows; and (3) monetary policy measures.

There is strong need and scope for further structural reforms. WEO analysis finds that labor and product

market reforms in advanced economies can give a strong boost to growth prospects over the medium

to long term. Carefully prioritizing and sequencing reforms is essential to boost their short-term effects.

Product market reforms—which aim to boost competition among firms and facilitate starting a

business or attracting investment—should be implemented forcefully, as they boost output even under

weak macroeconomic conditions and without weighing on public finances. Where possible, narrowing

unemployment benefits and easing job protection should be accompanied by other policies to offset their

short-term cost on vulnerable groups.

In many advanced economies, accommodative monetary policy remains essential to support economic

activity and lift inflation expectations. In many emerging market and developing economies, monetary

policy must grapple with the effects of weaker currencies on inflation and private-sector balance sheets.

Exchange rate flexibility, where feasible, should be used to cushion the impact of terms of trade shocks.

The WEO warns that policymakers also need to make contingency plans and design collective measures

for a possible future in case downside risks materialize. Cooperation to enhance the global financial safety

net and global regulatory regime is also central to a resilient international and financial system.

The IMF has warned that the recovery remains too slow and fragile, thus can damage the social and political

fabric of many countries. Also, persistent lower growth means less room for error, thereby reducing potential

output, and with it, demand and investment.

The current diminished outlook calls for a proactive response—not head-scratching and “more of the same.”

To support global growth, we need a more potent policy mix—a three-pronged policy approach based on

structural, fiscal, and monetary policies like the one the WEO proposes. If national policymakers were to

clearly recognize the risks they jointly face and act together to prepare for them, the positive effects on global

confidence could be substantial.

WT Wealth Management is a manager of Separately Managed Accounts (SMA). Past performance is no

indication of future performance. With SMA’s, performance can vary widely from investor to investor as each

portfolio is individually constructed and allocation weightings are determined based on economic and market

conditions the day the funds are invested. In a SMA you own individual ETFs and as managers we have the

freedom and flexibility to tailor the portfolio to address your personal risk tolerance and investment objectives

– thus making your account “separate” and distinct from all others we potentially managed.

An investment in the strategy is not insured or guaranteed by the Federal Deposit Insurance Corporation or

any other government agency.

Any opinions expressed are the opinions of WT Wealth Management and its associates only. Information is

neither an offer to buy or sell securities nor should it be interpreted as personal financial advice. You should

always seek out the advice of a qualified investment professional before deciding to invest. Investing in stocks,

bonds, mutual funds and ETFs carry certain specific risks and part or all of your account value can be lost.

In addition to the normal risks associated with investing, narrowly focused investments, investments in smaller

companies, sector ETF’s and investments in single countries typically exhibit higher volatility. International,

Emerging Market and Frontier Market ETFs investments may involve risk of capital loss from unfavorable

fluctuations in currency values, from differences in generally accepted accounting principles or from economic

or political instability that other nation’s experience. Emerging markets involve heightened risks related to the

same factors as well as increased volatility and lower trading volume. Bonds, bond funds and bond ETFs will

decrease in value as interest rates rise. A portion of a municipal bond fund’s income may be subject to federal

or state income taxes or the alternative minimum tax. Capital gains (short and long-term), if any, are subject

to capital gains tax.

Diversification and asset allocation may not protect against market risk or a loss in your investment.

At WT Wealth Management we strongly suggest having a personal financial plan in place before making

any investment decisions including understanding your personal risk tolerance and having clearly outlined

investment objectives.

WT Wealth Management is a registered investment adviser located in Scottsdale, AZ. WT Wealth Management

may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion

from registration requirements. Any subsequent, direct communication by WT Wealth Management with a

prospective client shall be conducted by a representative that is either registered or qualifies for an exemption

or exclusion from registration in the state where the prospective client resides. For information pertaining to

the registration status of WT Wealth Management, please contact the state securities regulators for those

states in which WT Wealth Management maintains a registration filing.

A copy of WT Wealth Management’s current written disclosure statement discussing WT Wealth Management’s

business operations, services, and fees is available at the SEC’s investment adviser public information website

– www.adviserinfo.sec.gov or from WT Wealth Management upon written request. WT Wealth Management

does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness,

or relevance of any information prepared by any unaffiliated third party, whether linked to WT Wealth

Management’s web site or incorporated herein, and takes no responsibility therefor. All such information is

provided solely for convenience purposes only and all users thereof should be guided accordingly