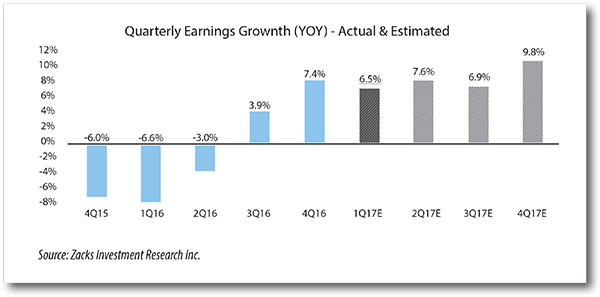

The first-quarter earnings reporting season is upon us. As of March 31, 2017, the

consensus estimate for Q1 2017 S&P 500 operating EPS was $29.17, up 9.9% on a

year-over-year basis (versus $26.54 in Q1 2016).

This advance would represent the third consecutive time the S&P 500 posted year-on-year EPS increases,

after enduring four successive declines. In addition, these results should lead to a new all-time 12-month high

of $120.32, eclipsing the prior high of $118.81 set in Q2 2015.

Furthermore, seven sectors are projected to see year-over-year increases, led by double-digit gains for

financials, information technology, and materials. What's more, energy's recent trough was set in Q1 2016, with

a loss of $0.35; yet Q1 2017 EPS is now seen at $3.07. Year-on-year EPS declines are expected to be reported

by the consumer discretionary, industrials, telecom services and utilities sectors. Finally, despite the expected

Q1 EPS increase, the S&P 500 trades are at a trailing 12-month operating P/E of 19.6X, or a 14% premium to its

median since 1988.

What will be the driving forces behind Q1's results? The following comments by equity research analysts we

follow concern the factors that likely affected EPS growth, including a 3% rise in the U.S. Dollar Index (Q1 2017

average vs. Q1 2016 average) and a 58% year-over-year surge in average quarterly WTI oil prices.

Most analysts have a relatively subdued outlook for Q1 EPS growth for this sector, which is expected to

record a 4.0% decline. Results for the media and entertainment space will be likely pressured by continued

investments in television programming and recent weakness in certain advertising categories, a potential

slowdown at the international box office, and some difficult comparisons for high-margin content licensing

revenues versus growth in subscriptions and affiliate fees.

Also, our outlook in part reflects likely margin pressures at traditional brick-and-mortar retail chains (versus

online-based ones) amid a continued post-holiday inventory clearance and rationalization, and hurt by soft

same-store sales trends and negative margin impact from rising online sales. We believe automotive margins

will be hurt by lower U.S. industry sales volume, increased incentive spending, and investment in autonomous

and mobility initiatives, offset by growth outside the U.S. and a favorable mix shift. Some lingering impact on

health concerns and labor cost inflation could also weigh on some restaurants and/or hospitality companies,

plus international expansion costs, including in Asia-Pacific and Europe.

Low-to-mid-teen revenue growth is expected in Q1 2017 for the homebuilders, driven by higher pricing and

scarcity of new homes in most markets. Affordability and mortgage-loan approvals remain on the watch list

but are not expected to be a problem for higher FICO-score households. Revenue growth will be driven by

higher volume within the "start-up" home category, though less from "move-up" or "luxury" product segments.

Despite rising labor and land costs, as well as narrowing gross margins, we believe that operating margins will

benefit from lower SG&A expenses. Finally, industry metrics, including average selling prices, unit orders and

deliveries, backlog volume, and value and community counts, should all show gains.

WT Wealth Management maintains an under-weight in this sector, as we believe that the sentiment of the

US consumer/shopper has changed, and that this sector offers more risk than reward, compared to others

available to us.

The consumer staples sector is expected to post a 2.9% rise in Q1 2017 EPS, as compared to a 9.9% increase

estimated for the S&P 500 and the 3.7% growth this sector experienced in all of 2016. We believe key factors

driving EPS growth underperformance in Q1 2017 for this sector are a shift in the Easter holiday into Q2 (from

Q1 in 2016), unseasonably warm weather, decreased demand from low-income families due to a delay in

receiving income-tax returns, persistent food deflation, demand pressures from higher year-over-year gasoline

costs, and ongoing drug reimbursement pressures.

However, we believe that growth was still achieved due to progress from ongoing cost savings initiatives

and improved pricing power in a more favorable global economic environment. We also see overall demand

benefiting as recent mergers, acquisitions and divestitures within the sector have led to improved exposure

to wider margin products, faster growing categories, and an expansion in distribution, thereby supplementing

greater scale advantages. Strong free cash-flow generation remains supportive of active share-repurchase

programs, in our view, which provides additional EPS growth support.

WT Wealth Management maintains a market weight in this sector. We believe that many of the larger Consumer

Staple names still have compelling yields, and that will aid in the attraction of capital and investor resources to

this sector. We believe there is "inherent safety" in many of these names, especially in light of what may turn

out to be less than anticipated GDP growth in the coming quarters.

The anticipated improvement in energy-operating EPS in Q1 2017 is deemed 'not meaningful,' or 'NM,' because

going to a positive from a negative renders any percentage calculations meaningless. Maybe this improvement

is best viewed in terms of a recovery. After all, the sector has turned the corner, and what had been negative

EPS in Q1 2016 is now likely to be a modest gain in Q1 2017, in part because: (a) crude oil prices are considerably

better this time around, and (b) energy companies have had a year to work on further cost-efficiency efforts.

The upstream space, which dominates the market cap of the S&P 500 energy value chain and benefits from

higher crude prices, will be relatively better off, for West Texas Intermediate (WTI) averaged about $33 per

barrel in Q1 2016 and should be in the high $40 or low $50-per-barrel range in Q1 2017. Customers are beginning

to spend again, and consensus estimates point to a 16% recovery in upstream capex in 2017, which, if realized,

should be the first uptick after two down years. And that new customer spending supports the drillers' and oil

services' names.

Our wariness on energy stems from our concern that, while these changes are in a positive direction, they are

insufficient to bring the sector back to its heydays in the 2011-2014 time frame, and valuations in many areas

remain stretched. If we had to "pick" our favorite space within energy today, it would be in midstream – the

pipeline space, where a 'Goldilocks' price for crude is enough to drive higher customer spending on projects,

supported by a Trump administration that sees red wherever it finds red tape, but not so high that it kills

demand.

WT Wealth Management maintains an under-weight in the energy sector, where we believe the risks greatly

outweigh the rewards.

In the aggregate, the S&P 500 financials sector is projected to record the second-highest EPS gain in Q1 2017.

This will be led by the investment banking & brokerage area, which is expected to record strong double-digit

revenue growth from capital markets in both equity and fixed income trading areas, as investment banking

got a boost in advisory fees for IPOs, and M&A provided continued growth in that market.

Wealth and asset management companies should show revenue gains, but not like those in Q4 2016, when

the equity market rose strongly. Net interest income is expected to have risen along with higher rates, which

benefit banks on deposits, as well as brokerage firms on investment accounts. Operating income margins

are expected to have widened from higher revenues, because there were no major changes in key cost

items, such as compensation. Because some discount brokers derive nearly half their revenue base from net

interest income, a higher-rate environment will propel revenues by double digits. However, the newly initiated

commission price war will affect some of the second-tier players.

Revenue growth is projected to be modest for life insurers, due to weak annuity sales amid regulatory

uncertainty that should be offset by growth in headcount-driven products as a result of favorable labor

market trends. Higher interest rates should drive net investment income and help to widen operating margins,

particularly on existing books of spreads-based businesses.

Many life insurers will continue to boost EPS growth through share buybacks, even though regulatory uncertainty

related to the DOL fiduciary rule and SIFI designations continue to inject a degree of unpredictability into this

group.

We expect top-line growth of 3-4% for the P/C insurers on 2-3% growth in premiums and higher ratedriven

investment income. We expect operating margins to remain under some pressure from deterioration

in underwriting results. However, things are not bad enough to spark a turn in pricing, so this group will

likely continue to muddle along. Some of the more facile reinsurers may produce above-average results; the

reinsurance space has been consolidating, which will help buoy valuations.

WT Wealth Management maintains an over-weight in the financial service and regional banking sector. Even if

the Federal Reserve's goals of 3% rate increases in 2017 and 3% in 2018 miss the mark, we cannot believe that

interest rates will not be higher in 6-12 months, which bodes well for financials and regional banks.

The healthcare sector has experienced significant

recent volatility, primarily due to the possible repeal

and replacement of the Affordable Care Act (ACA).

The withdrawal of the House Republicans' health care

proposal, called the American Health Care Act, due to

an insufficient amount of votes to pass the bill caused

this sector even more volatility.

However, despite all of the "noise," the volatility has no

immediate impact on the sector's current earnings. Q1

typically is a softer quarter for healthcare, mainly due

to a reset of deductibles that result in lower physician

visits, hence lower healthcare services and drug sales,

etc. We do not anticipate any material change this

year, which is reflected in the modest 0.4% earnings

growth forecast.

We are encouraged by several positive clinical trial

data readouts and recent drug approvals that should

aid drug sales later this year and the next year.

This is welcome news for the biotechnology and

pharmaceutical industries, which are on the heels of only 22 new drugs approved in 2016 (45 and 41 new drugs

were approved in 2015 and 2014, respectively). However, we still anticipate only flat-to-modest growth for the

drug sector, as we see continued pricing pressure in the generic space and ongoing scrutiny on high drug

prices for branded drugs, limiting sales growth. We look for improved earnings for the larger health insurers,

as they significantly reduced their participation in the public healthcare exchanges that hurt profitability over

the last two years.

WT Wealth Management currently maintains an over-weight in the healthcare sector. We believe that the

imminent failure of the ACA and the increasing aging of the American population make this a compelling

sector in the years ahead.

Q4 2016 EPS were relatively muted for most of the companies in the industrial sector. Standouts were in: (a)

industrial machinery and tools, where demand was strong; (b) equipment rentals, where demand firmed up

nicely; and (c) air freight and logistics, where demand was also strong, but costs increased faster.

The revenue outlook is relatively weak for defense companies. Defense budgets have not actually increased

yet, but statements from the Trump administration indicate a likely improved revenue outlook over the next

few years. The aerospace area remains strong, but backlogs have declined somewhat. EPS strength was driven

by a work-down of current strong backlogs, which remain robust but were culled slightly.

Airlines saw the pricing environment strengthen but were more adversely affected by higher fuel costs. Oil

has weakened some since the end of Q4 2016, however, which should help Q1 2017 results. Rails have seen

improving commodity volumes in many areas off a weak base, especially in coal, which rebounded in Q4 2016.

We believe that the EPS was good for this category in Q1 2017, aided by streamlined costs and better volumes.

Trucking remains challenged by industry overcapacity, which impacted Q4 EPS. Volumes improved, however,

and the companies mostly beat EPS expectations. Finally, conglomerates remain hampered by their ties to

energy, and, though oil prices have risen, project delays seem to continue. Revenue growth is expected to be

in the low single digits at best, but we should see some acceleration in Q1 and the rest of 2017.

WT Wealth Management maintains an over-weight in the Industrial sector. We believe that the rewards

outweigh the risks here, and that infrastructure and defense spending will see greater funding and benefits in

the years ahead. We believe that this sector will not be free of volatility and will trade just as much on rhetoric

and news as it does on fundamentals. So one will need discipline, a strong stomach, and patience to see the

rewards.

INFORMATION TECHNOLOGY (IT)

According to consensus estimates, Q1 EPS for the S&P 500

technology sector should post the strongest growth, up 16.5%

compared to the prior-year period. S&P 500 EPS is projected

to rise 9.9%. We see the January-to-March period as relatively

important for most technology companies, following the

critical Q4, including consumers making purchases during

the holiday shopping season and corporations spending

what is left within technology budgets.

The U.S. dollar influences the financial results of S&P 500 IT

sector companies, given their substantial exposure to foreign

sales. Increases in the dollar versus international currencies

make U.S. products and services relatively more expensive

for purchase in other currencies. For 2015 (latest available),

per S&P Dow Jones Indices, the technology sector generated

58% of revenues from international sources – the second

most of the 10 economic sectors – compared with 44% for

the S&P 500. The profits on non-U.S. revenues also tend to be

relatively high, given generally lower tax obligations abroad.

Notably, in Q1 2017, after significant appreciation following the U.S. elections in November, the U.S. dollar fell

against major global currencies, including the Euro and the Japanese Yen. We also believe that consumer and

corporate confidence is relatively high, and may have aided purchases in Q1 2017.

WT Wealth Management maintains an over-weight in this sector, as technology sectors like IT are the railroads

of 75 years when it comes to their importance and entrenchment in American culture.

The materials sector is projected to record its third-highest Q1 EPS

growth, at 13.5%. Chemical companies are benefiting from higher

prices and rising global demand for their products.

Fertilizer and agricultural chemical companies are benefiting

from rising corn prices, which in turn are boosting prices of seed,

nitrogen, phosphates and potassium. Strong fertilizer demand

in Brazil is helping as well. Higher oil prices are benefiting the

commodity chemical-oriented companies, and we see continued

strength in specialty chemical companies driven by rising demand

and higher prices. Steel producers are benefiting from higher

year-over-year steel prices and higher mill-utilization, driven by

continued improvements in nonresidential construction demand.

Partly offsetting the strength in steel producers, Freeport-McMoRan

should weigh negatively on the group, given the unpredictable

outcome of its Grasberg mine in Indonesia.

WT Wealth Management maintains a market-weight in the materials sector. Even with considerable bullish

sentiment, we believe that many issues we are unable to predict, such as currency evaluations, could adversely

affect the materials sector in the coming months.

Rental rates across most property types are expected to record low-to-mid single-digit growth year over year.

Occupancy rates remain near all-time highs within industrial, multi-family and office markets but are easing in

self-storage and hotel property types. Real estate investment growth is beginning to ease from higher levels in

2015 and 2016, and property acquisitions will remain well below normal levels, given competition from foreign

buyers such as China. However, dividend growth is on track for 2017, with available cash and FFO growth.

Consensus estimates point to a below-market growth for the sector in Q1 EPS, particularly for retail REITS,

as a rash of announced and planned retail store closings, coupled with the impact higher interest rates have

on REIT stock performance, offset the positive factors of industrywide net absorption of space and favorable

macro trends. However, we believe that a handful of these retail REITs, particularly those with Internet-resistant

retail tenants, could surprise on the upside.

WT Wealth Management sees considerable risk in the real estate sector, despite somewhat bullish sentiment

from many analysts. The headwind of rising interest rates, the death of brick-and-mortar retail, and the stilldubious

sustainable GDP growth would lead us to look elsewhere other than real estate for capital appreciation

and yield opportunities.

TELECOMMUNICATION SERVICES

The S&P 500 telecommunications services sector, according to S&P Capital IQ consensus estimates, is expected

to generate a Q1 EPS decline of 2.1%. We expect revenue pressure to remain, given fierce competition from

carriers. However, we believe that broadband growth and cost savings will preserve free cash-flow generation

and support dividends. We note that AT&T and Verizon together comprise more than 90% of the S&P 500

Telecom Index.

We see an ongoing consumer sentiment shift toward value-service providers, such as T-Mobile and Sprint,

given their lower costs, unlimited data options, improving networks, and availability of leasing options. We

note that both of these carriers once again likely outstripped their larger peers in postpaid phone subscriber

gains in Q1.

However, the recent unlimited data plans both Verizon and AT&T announced in Q1 2017 could have negative

implications on industry pricing for the remainder of the year. We believe that competition between the largest

wireless providers will remain intense and will focus on expanding offerings in such areas as the connected car

and over-the-top space.

In wireline, we expect continued access-line weakness but stable broadband subscriber gains. Competitive

threats from cable and satellite providers should weigh on pricing and subscriber growth. However, we see

continued cost-cutting, merger synergies, and business market improvements supporting free cash-flow.

In light of that, smaller providers may cut/reduce existing attractive dividends, given a rising interest-rate

environment, execution issues from recent acquisitions, and elusive growth prospects.

Finally, we see the telecommunications services sector being impacted by modest U.S. economic growth

and still favorable, albeit rising, interest rates. For the S&P 500 Telecom space, we believe that free cash-flow

generation from the bellwether telecom providers (AT&T and Verizon) will be enough to support an attractive

dividend yield (over 4.5%) for the sector.

WT Wealth Management maintains a market-weight in the telecommunications sector. We are more bullish

than many in this area and acknowledge that this could be an interesting and convoluted space, but just look

around: hardly any Americans, or earthlings, are not intimately attached to their mobile phones – which we

believe will ultimately lead to compelling opportunities within this space.

Overall temperatures across the U.S. were slightly warmer in Q1 2017

than in the same period last year. However, it was much warmer in

the Southern states. Since electric home and space heating is much

more prevalent in the South, this should adversely affect electric

demand and revenues.

However, in the densely populated Northeast, temperatures were in

line with the national average. Oregon and Washington state were

much colder than average, but, given a lack of S&P 500 utilities in

those areas, we see little impact on the sector's Q1 2017 results.

Partly offsetting the negative temperatures, we see customer

growth and rate increases positively affecting revenues. Costreduction

efforts and share repurchases should partly offset the

slightly lower revenues, leading to a small decline in EPS.

WT Wealth Management had been very over-weighted in these

sectors until we adopted the Trump-trade several days after the

presidential election. We believed that stronger, more compelling opportunities were presented in many areas,

including financials, technology, semi-conductors, and industrials. Today we have a market-weighting in the

sector, and we still believe it is a good area for safe, compelling dividend yields.

So there you have it – the recovery from the 2015-16 EPS recession continues, as the S&P 500 is expected to

report the first in a series of near-double-digit gains. Financials, information technology, and materials sectors

are expected to show the greatest growth, while consumer discretionary, industrials, telecom services and

utilities post year-over-year declines.

However, history implies that the final tally will be even better, as in each of the last 20 quarters actual EPS

exceeded initial estimates and have done so by an average of 3.5 percentage points. Therefore, Q1 EPS growth

may actually post a near-13.5% gain. This should assist in validating post-election optimism, which has pushed

valuations to lofty levels.

We have been the first to acknowledge that the current rally and increase in equity valuations have all been

on hope and promise. As of this writing, the Trump administration has not done anything other than boosting

hope and optimism in the business-owner, and it is difficult to measure the impact on the hundreds of Obamaera

regulations that have been squashed via executive order.

While we always refrain from being political, we do wish the new administration had tackled tax reform,

spherically the re-repatriation of the hundreds of billions of dollars still parked overseas by American

corporations. Ultimately, the lack of growth in this country over the past several years has been due to high

tax rates, general unfriendliness in the business climate, and unwillingness of companies to invest domestically

for a litany of reasons.

Overall, we still believe that this market has room to move, Q1 2017 earnings will meet expectations, and

guidance will be encouraging but cautious. Earnings season will not be without volatility, but at WT Wealth

Management we believe we own many of the best companies that have wide moats and huge market shares

and have entrenched themselves so deeply into the American lifestyle they have become the "new" blue chips

of today.

WT Wealth Management is a manager of Separately Managed Accounts (SMA). Past performance is no indication

of future performance. With SMA's, performance can vary widely from investor to investor as each portfolio is

individually constructed and allocation weightings are determined based on economic and market conditions

the day the funds are invested. In a SMA you own individual ETFs and as managers we have the freedom and

flexibility to tailor the portfolio to address your personal risk tolerance and investment objectives – thus making

your account "separate" and distinct from all others we potentially managed.

An investment in the strategy is not insured or guaranteed by the Federal Deposit Insurance Corporation or any

other government agency.

Any opinions expressed are the opinions of WT Wealth Management and its associates only. Information is neither

an offer to buy or sell securities nor should it be interpreted as personal financial advice. You should always seek

out the advice of a qualified investment professional before deciding to invest. Investing in stocks, bonds, mutual

funds and ETFs carry certain specific risks and part or all of your account value can be lost.

In addition to the normal risks associated with investing, narrowly focused investments, investments in smaller

companies, sector ETF's and investments in single countries typically exhibit higher volatility. International,

Emerging Market and Frontier Market ETFs investments may involve risk of capital loss from unfavorable

fluctuations in currency values, from differences in generally accepted accounting principles or from economic or

political instability that other nation's experience. Emerging markets involve heightened risks related to the same

factors as well as increased volatility and lower trading volume. Bonds, bond funds and bond ETFs will decrease in

value as interest rates rise. A portion of a municipal bond fund's income may be subject to federal or state income

taxes or the alternative minimum tax. Capital gains (short and long-term), if any, are subject to capital gains tax.

Diversification and asset allocation may not protect against market risk or a loss in your investment.

At WT Wealth Management we strongly suggest having a personal financial plan in place before making any

investment decisions including understanding your personal risk tolerance and having clearly outlined investment

objectives.

WT Wealth Management is a registered investment adviser in Arizona, California, Nevada, New York and

Washington with offices in Scottsdale, AZ Jackson, WY and Las Vegas, NV. WT Wealth Management may only

transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration

requirements. Individualized responses to persons that involve either the effecting of transaction in securities, or

the rendering of personalized investment advice for compensation, will not be made without registration or

exemption. WT Wealth Managements web site is limited to the dissemination of general information pertaining

to its advisory services, together with access to additional investment-related information, publications, and links.

Accordingly, the publication of WT Wealth Management web site on the Internet should not be construed by

any consumer and/or prospective client as WT Wealth Management solicitation to effect, or attempt to effect

transactions in securities, or the rendering of personalized investment advice for compensation, over the Internet.

Any subsequent, direct communication by WT Wealth Management with a prospective client shall be conducted

by a representative that is either registered or qualifies for an exemption or exclusion from registration in the

state where the prospective client resides. For information pertaining to the registration status of WT Wealth

Management, please contact the state securities regulators for those states in which WT Wealth Management

maintains a registration filing. A copy of WT Wealth Management's current written disclosure statement discussing

WT Wealth Management's business operations, services, and fees is available at the SEC's investment adviser

public information website – www.adviserinfo.sec.gov or from WT Wealth Management upon written request. WT

Wealth Management does not make any representations or warranties as to the accuracy, timeliness, suitability,

completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to WT

Wealth Management's web site or incorporated herein, and takes no responsibility therefor. All such information

is provided solely for convenience purposes only and all users thereof should be guided accordingly