Click here to download the PDF

Given 2017's impressive returns on the equity market, one might have expected that

SmallCap stocks-typically high-risk, high-return investments-would have risen at

least as much as their LargeCap counterparts. But that was not the case. SmallCap stocks, as represented in

the Russell 2000 Index, returned only 14.6% in 2017, well shy of the 21.64% performance of the S&P 500.

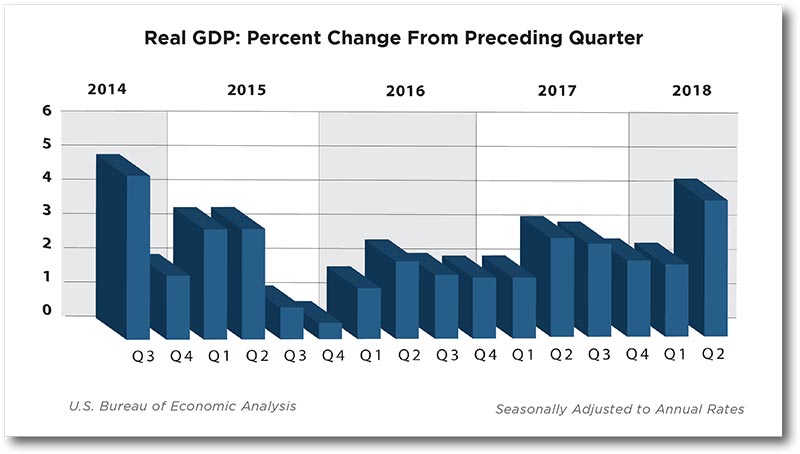

Momentum certainly remained with the larger companies as we entered 2018. The S&P 500 returned 5.62% in

January of this year, only to suffer a natural correction and give back 3.89% and 2.69% in February and March,

respectively.

In light of trade war concerns and increased U.S. dollar volatility, more investors sought out smaller domestic

public companies that seem to provide a shield against world economic fluctuations and the corresponding

headline news of LargeCap multi-nationals. Multi-nationals, found in the Dow Jones Industrial Average, have

suffered the most in this environment while smaller cap, more domestically focused SmallCaps faired the best.

- The S&P 500® was up 3.03% in August, bringing the YTD return to 8.52%.

- The Dow Jones Industrial Average® gained 2.16% for the month and was up 5.04% YTD.

- The S&P MidCap 400® was up 3.03% for the month and up 7.58% YTD.

- The S&P SmallCap 600® was up 4.72% in August and up 17.31% YTD.

FactSet data reported that investors in exchange-traded funds (ETFs) have recently turned away from

LargeCaps, pulling some $20 billion out of LargeCap ETFs in June alone. SmallCap ETFs appeared to be a

major beneficiary of these outflows as we examine monthly equity flow and allocation data.

Below we examine some of the forces spurring investors to consider SmallCaps.

Protections from Trade Wars

The current administration's tariffs on aluminum and steel have caused investors to spurn LargeCap companies

that have hefty international exposure, where an impending trade war with China or other countries will affect

profits and revenue more significantly. On the other hand, American SmallCap stocks tend to generate revenue

through domestic markets, so they are more impervious to world trade policy conflicts.

The Rising Dollar

The continuing rise of the U.S. dollar is adversely affecting domestic equities, but many smaller U.S. companies

are again more insulated from the impacts of a rising dollar because most of their sales come from domestic

markets. Larger firms, on the other hand, tend to have significant international operations, which a rising U.S.

dollar can negatively affect.

Companies in the S&P SmallCap 600 derive 78.8% of their revenue from U.S. consumers, compared with 73.3%

in the S&P MidCap 400 and 60.9% in the S&P 500. Historically, SmallCap stocks have weathered geopolitical

turmoil and currency fluctuations more effectively than LargeCap equities.

A Less Taxing Environment

SmallCap firms usually pay higher effective taxes and have greater compliance obligations, so tax reform and

deregulation would likely be an asset to them. Furthermore, earnings that were formerly generated abroad by

LargeCap companies were held in foreign nations as a tax shelter.

This year, off-shore balances will be subject to a one-time tax of 15.5%. That cash can be used in various ways,

mostly likely acquisitions, dividend increases and stock buy backs. Small companies will be most attractive

for acquisition, so this tsunami of cash returning to American shores may especially bolster SmallCap equity

pricing.

Many analysts agree that U.S. SmallCap and MidCap public companies are better positioned for a boost from

the corporate tax cuts than are most LargeCap firms in the S&P 500. Russell 2000 firms have paid at least $9.2

billion less in taxes in the second quarter of 2018 than in the last quarter of 2017, Reuters reported. SmallCap

firms have shown a propensity to reinvest those savings over stock buybacks, in contrast to LargeCap firms.

Growth Abounds

U.S. economic growth got off to a slow start in 2017 with Q1 GDP at just 1.8%. The final 3 quarters of 2017 then

grew to more appropriate levels with Q2 at 3%, Q3 at 2.8% and Q4 at 2.3%

We anticipate domestic and global GDP will remain healthy through 2018 and corporate profits will be broadbased.

SmallCap firms, catering to a domestic audience, have growth opportunities from both household

and government spending (the latter may include an impending infrastructure bill), in addition to easy-credit

conditions and business capital expenditure environment.

SmallCap equities may also be advantageous over LargeCap equities in respect to currency effects. A more

hawkish Federal Reserve, rising bond yields, and above-trend rates of economic growth may push the dollar

higher, relative to our trade partners. A higher-value dollar cheapens producer inputs, which decreases costs

for domestic companies that import parts or raw materials. However, a higher-value dollar also increases

prices on U.S. products in global markets. On both counts, LargeCap companies, with significant production

and earnings generation outside of the U.S., are at a comparative disadvantage to SmallCap companies which

do not have the same global reach and dependency.

SmallCap stocks should be a measured component of a strategic asset allocation strategy in most market and

economic cycles. However, they can have additional volatility over LargeCap equities.

WT Wealth Management's proprietary research has shown that there are distinct periods when owning

SmallCap companies are better than at other times. Traditionally, the best time to hold and increase SmallCap

stock allocations has been early in the economic recovery cycle. One reason for this is SmallCap companies

can react and adapt more quickly to improved economics and traditionally outperform LargeCap companies which are like battleships and can require more "ramp up time" as the economy exits a recession and enters

an economic recovery/expansion phase. Smaller companies can be more like speedboats; agile and quick to

respond.

However, our present economic environment is anything but traditional. We are deep into one of the longest,

slowest economic expansions in modern times. Since the "great bottom" in the S&P 500 on March 2, 2009,

where it stood at 638.38, we have steadily climbed to 2,901.52, a 264% return. Come early next year, we expect

the current expansion to celebrate a 10-year anniversary.

Then why look at SmallCaps now when we appear to be so late in the economic cycle? When you couple low

interest rates, a strong economy, generational corporate tax cuts, unprecedented deregulation and a trade

war, it is definitely worth evaluating SmallCap allocations in the current environment, which appears favorable

to such companies. This is clearly a tactical allocation call and could be short or long lived.

We understand that every investor is special and unique. Please consult your financial advisor to determine

if an allocation to SmallCaps is appropriate for your portfolio, considering your overall investment objectives,

time horizon and tolerance for account fluctuations.

Chang, Ellen. "A Rising Dollar Can Impact Equities Negatively." U.S. News & World Report, June 20, 2018

View Source

Clarke, Courtney. "Strong Small-Cap Equity Market Attractive to Investors." Miles Capital, June 28, 2018.

View Source

Constable, Simon. "How Trade War Fears are Boosting Small Caps." Forbes, July 23, 2018.

View Source

Kawa, Luke. "U.S.-Centric Stocks are Losing Their Immunity to Trade Wars." Bloomberg, June 26, 2018.

View Source

Randall, David. "Tax Cut Helping Turn U.S. Small Caps Into Unlikely Source of Safety." Reuters, May 10, 2018.

View Source

Serenbetz, Robert. "Five Potential Benefits for Small Caps." New York Life Investments Blog, January 24, 2018.

View Source

Talbot, Bill. "How Small-Cap Stocks May Benefit from the New Tax Law." John Hancock Investments, January 12, 2018.

View Source

WT Wealth Management is an SEC registered investment adviser, with in excess of $100 million in assets under management

(AUM) with offices in Flagstaff, Scottsdale and Sedona, AZ along with Jackson Hole, WY and Las Vegas, NV.

WT Wealth Management is a manager of Separately Managed Accounts (SMAs). With SMAs, performance can vary widely

from investor to investor as each portfolio is individually constructed and managed. Asset allocation weightings are

determined based on a wide array of economic and market conditions the day the funds are invested. In an SMA, each

investor may own individual Exchange Traded Funds (ETFs), individual equities or mutual funds. As the manager we have

the freedom and flexibility to tailor the portfolio to address an individual investor's personal risk tolerance and investment

objectives – thus making the account "separate" and distinct from all others we manage.

An investment with WT Wealth Management is not insured or guaranteed by the Federal Deposit Insurance Corporation

(FDIC) or any other government agency.

Any opinions expressed are the opinions of WT Wealth Management and its associates only. Information offered is neither

an offer to buy or sell securities nor should it be interpreted as personal financial advice. Always seek out the advice of

a qualified investment professional before deciding to invest. Investing in stocks, bonds, mutual funds and ETFs carries

certain specific risks and part or all of an account's value can be lost.

In addition to the normal risks associated with investing, narrowly focused investments, investments in smaller companies,

sector and/or thematic ETFs and investments in single countries typically exhibit higher volatility. International, Emerging

Market and Frontier Market ETFs, mutual funds and individual securities may involve risk of capital loss from unfavorable

fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political

instability that other nations experience. Individual bonds, bond mutual funds and bond ETFs will typically decrease in

value as interest rates rise. A portion of a municipal bond fund's income may be subject to federal or state income taxes or

the alternative minimum tax. Capital gains (short and long-term), if any, are subject to capital gains tax.

Diversification and asset allocation may not protect against market risk or investment losses. At WT Wealth Management, we

strongly suggest having a personal financial plan in place before making any investment decisions including understanding

personal risk tolerance, having clearly outlined investment objectives and a clearly defined investment time horizon.

WT Wealth Management may only transact business in those states in which it is registered, or qualifies for an exemption

or exclusion from registration requirements. Individualized responses to persons that involve either the effecting of

transactions in securities, or the rendering of personalized investment advice for compensation, will not be made without

registration or exemption. WT Wealth Management's website is limited to the dissemination of general information

pertaining to its advisory services, together with access to additional investment-related information, publications, and

links.

Accordingly, the publication of WT Wealth Management's website should not be construed by any consumer and/or

prospective client as WT Wealth Management's solicitation to effect, or attempt to effect transactions in securities, or the

rendering of personalized investment advice for compensation, over the internet. Any subsequent, direct communication

by WT Wealth Management with a prospective client shall be conducted by a representative that is either registered or

qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

A copy of WT Wealth Management's current written disclosure statement discussing WT Wealth Management's registrations,

business operations, services, and fees is available at the SEC's investment adviser public information website (www.

adviserinfo.sec.gov) or from WT Wealth Management directly.

WT Wealth Management does not make any representations or warranties as to the accuracy, timeliness, suitability,

completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to WT Wealth

Management's web site or incorporated therein, and takes no responsibility therefor. All such information is provided solely

for convenience purposes and all users thereof should be guided accordingly.