President Trump's most recent executive order – calling on the Treasury Department to review its rules for

required minimum distributions (RMDs) from 401(k) plans and IRAs – was met with mixed reviews.

Generally, under current rules, investors must start to withdraw funds from qualified retirement accounts when

they turn 70½ and pay taxes on those distributions as ordinary income. Remember also that an investor

with a tax-favored retirement account is permitted to begin taking distributions as early as 59½. RMDs don't

have any effect on that allowance. Rather, RMDs simply require someone who has elected to delay their

allowable distributions to start taking them at some point. But is 70½ the right age for RMDs to start? Should

distributions be postponed by 6, 7, 10 years or even eliminated?

HOW IMPORTANT IS THE RMD ISSUE?

Beginning in 2016, when the first of the baby boomer generation reached 70½, a growing share of applicable

retirement savings had become subject to RMDs, the minimum amount that the holder of a retirement plan

account is required to withdraw starting in the year that person reaches age 70½. As a result, throughout the

next 20 years, billions of dollars annually will be forced from retirement accounts through distributions that

will, in many cases, be taken in the form of a single large annual payment. While RMDs have been mandated

for decades, the number of baby boomer retirees is steadily increasing, along with the magnitude of their

accrued retirement assets since the Great Recession of 2008-2009 decline. This trend will certainly intensify

the effects of retirement withdrawals once these people hit 70½.

HOW WE ARRIVED AT TODAY'S RMD REALITY

The increase in number of defined contribution plans came about from the congressional passage of multiple

acts throughout the 1970s and 1980s, such as the Employee Retirement Income Security Act and the Revenue

Act of 1978. These acts allowed employees more flexibility and control over the amounts and frequencies

of funding their IRAs beyond mere dependence on their places of employment for their retirement income.

Consequently, IRA funding responsibility often shifted from one's employer to the employees themselves.

Yet the increase in defined contribution plan assets seemed to indicate that taxpayers were using them as taxfree

income cash cows as opposed to fair retirement income channels. In response, the Tax Reform Act of 1986

dictated that taxpayers must start to receive annual distributions from their tax-deferred defined contribution

plans beginning at age 70½.

The majority of retirement accounts are regulated by the RMD rule: RMDs must be taken from SEPs, SARSEPs,

SIMPLE IRAs, SEP IRAs, and other conventional IRAs and IRA-based retirement plans. Employer sponsored

plans, including profit-sharing 401(k), 403(b) and 457(b) plans, also fall under the RMD rule's jurisdiction.

ASSETS IN SCOPE AND RMD CALCULATIONS

The Investment Company Institute (ICI) reported that U.S. retirement assets totaled $24.7 trillion by the close

of 2017, of which $8.4 trillion were found in employer-sponsored defined benefit plans and state, federal and

local government plans. The remaining $16.3 trillion were in assets subject to RMDs: IRAs had $7.4 trillion;

defined contribution plans had $6.8 trillion; and annuities had $2 trillion.

RMDs are calculated with IRS-published Distribution Period tables based on the end-of-the-year balance of

the retirement asset subject to required minimum distributions. The mandated minimum withdrawal amount is

calculated by dividing the asset's balance from the end of the previous year by the Distribution Period factor

for the account owner's age at the time the distribution occurred. The quotient is the amount of the owner's

minimum mandated distribution for the present tax year.

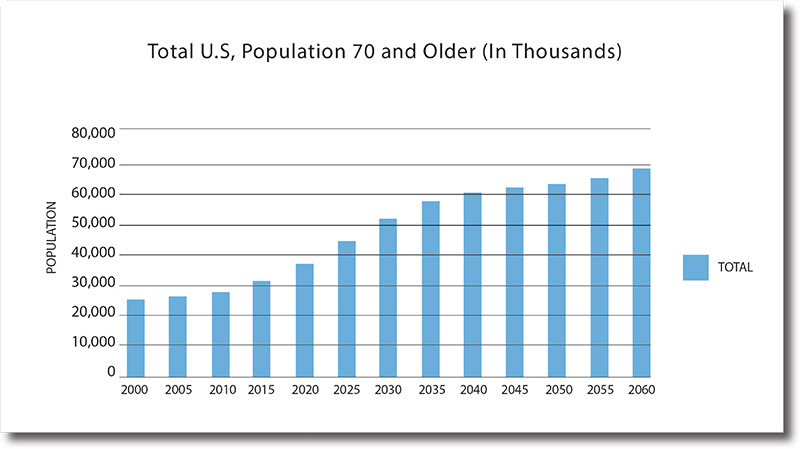

THE POPULATION TRAJECTORY – AGE 70+

Individuals aged 70+ numbered about 25.5 million in 2000, according to the US Census Bureau (Fig. 2).

Increased by 24% by 2015, this population now numbers 31.7 million and is predicted to reach 37.9 million in

the next several years and 58.7 million by 2035. After leveling off after 2035, the population is anticipated to

peak again in 2060 at 69 million.

The projected population growth of people aged 70+ over the following 45 years is also charted here.

THE DEBATE AROUND PRESIDENT TRUMP'S PROPOSED CHANGE

Some say 70½ is too soon for RMDs, as many baby-boomers keep working well into their 70s, and thus don't

need the retirement cash right away. Others warn that an RMD age increase could cause a revenue deficit for

the government, as less tax revenue would be coming in.

The oldest of the 75 million baby boomers in the U.S. turned 70½ in July of 2016, so we are just at the beginning

of the age wave, which means much will be extracted from retirement accounts over the coming decades. This,

combined with higher life-expectancy rates, has prompted many to call for increasing or even eliminating the

RMD age so seniors can control their retirement assets more efficiently.

In our opinion, age 70½ is far too soon for forced withdrawals from tax-favored retirement accounts. At WT

Wealth Management, we have many clients who are dismayed at having to start taking withdrawals at that age

before they really need that money. Some are still working, because they love their careers, are in good health,

and fear physical and/or mental declines if they slow down. These clients are forced to take the required withdrawal

and pay the taxes on it, but they uniformly reinvest the remaining proceeds in a non-qualified

account. The only reason they're taking the money out in the first place is because they're required to. If

they were not, the money could remain in their tax-deferred accounts and possibly be passed on to their

beneficiaries.

IRS life expectancy tables were last updated in April 2002. Since then, data from the Federal Reserve Bank

of St. Louis show that Americans have been living longer, with the average American life expectancy rising to

about 78½ years from below 77 in 2002. So we believe that the RMD age should be raised to 75, or even 78, to

reflect longevity and work continuation trends. (Case in point: Warren Buffett, age 88.)

In fact, we believe that no one who is still working should be forced to pull money out of a tax-favored

retirement account. When combined with a regular paycheck, these distributions can cause taxable income

to balloon significantly, thus putting some seniors into higher tax brackets, reducing their tax benefits, and

sticking them with higher tax bills that deplete retirement balances.

This could be partially resolved by increasing the RMD age to 78, as fewer seniors tend to work into their 80s,

and those no longer working in their 70s would have more leeway to plan their withdrawals according to their

individual financial goals, including tax reductions and deferments for the subsequent generation.

Yet changing the required timing for RMDs could also affect the level of tax revenue coming into the federal

government. At the very least it delays it. Depending on tax brackets it could even reduce it. So it's a little

surprising that President Trump would propose changing or eliminating this requirement in light of the 2018

tax cuts, a continued budget deficit, and $21 trillion in US debt.

True, RMDs were a compromise we had to accept when we began to place money in tax-deferred retirement

accounts. But tax revenue will not be significantly affected, mostly just deferred, by an RMD age increase. The

income tax bill never goes away since IRAs or 401(k)s do not have the step-up in tax basis at death like non

qualified retirement funds and other assets do. Whoever withdraws the taxable IRA or other retirement funds

will pay the income tax whenever it is withdrawn.

And finally, when we say the U.S. should raise the RMD age to 75 or 78, we don't mean 75½ or 78½. The U.S.

government should make the RMD age one that everyone can easily understand.

Brandon, Kyle.SIFMA Research Quarterly, Fourth Quarter 2017, Research Report.

New York and Washington, D.C.: Securities Industry and Financial Markets Association, 2017.

View Source

Carrns, Ann. "If You're 70½, It's Time to Take Money From Your Retirement Account."

The New York Times, December 1, 2017.

View Source

Edwards, Chris. "Tax Reform: Ending Forced Retirement Withdrawals."

Cato Institute, October 17, 2017.

View Source

Internal Revenue Service.

"Retirement Plan and IRA Required Minimum Distributions FAQs."

IRS.gov. Updated May 30, 2018.

View Source

Longo, Tracy.

"Trump Calls For Review Of Rule Requiring RMDs At 70½."

Financial Advisor, August 31, 2018.

View Source

O'Brien, Sarah.

"Trump order seeks to ease retirement account rules for required withdrawals."

CNBC, August 31, 2018.

View Source

Shane, Edward.

"Baby Boomers and Required Minimum Distributions: Preparing for the Big Wave of Asset Outflows."

BNY Mellon, March 2016

View Source

Shane, Edward.

"The Impending Convergence of Baby Boomers and Required Minimum Distributions."

BNY Mellon | Invested. New York: The Bank of New York Mellon Corporation, 2016.

View Source

"Should the U.S. Raise the Age for Mandatory IRA Withdrawals?"

The Wall Street Journal, March 19, 2017.

View Source

Slott, Ed, and Robert L. Meyer.

"Should the US Raise the Age for Required IRA Distributions?"

MarketWatch, April 1, 2017.

View Source

WT Wealth Management is an SEC registered investment adviser, with in excess of $100 million in assets under management

(AUM) with offices in Flagstaff, Scottsdale, Sedona and Tucson, AZ along with Jackson Hole, WY and Las Vegas, NV.

WT Wealth Management is a manager of Separately Managed Accounts (SMAs). With SMAs, performance can vary widely

from investor to investor as each portfolio is individually constructed and managed. Asset allocation weightings are

determined based on a wide array of economic and market conditions the day the funds are invested. In an SMA, each

investor may own individual Exchange Traded Funds (ETFs), individual equities or mutual funds. As the manager we have

the freedom and flexibility to tailor the portfolio to address an individual investor's personal risk tolerance and investment

objectives – thus making the account "separate" and distinct from all others we manage.

An investment with WT Wealth Management is not insured or guaranteed by the Federal Deposit Insurance Corporation

(FDIC) or any other government agency.

Any opinions expressed are the opinions of WT Wealth Management and its associates only. Information offered is neither

an offer to buy or sell securities nor should it be interpreted as personal financial advice. Always seek out the advice of

a qualified investment professional before deciding to invest. Investing in stocks, bonds, mutual funds and ETFs carries

certain specific risks and part or all of an account's value can be lost.

In addition to the normal risks associated with investing, narrowly focused investments, investments in smaller companies,

sector and/or thematic ETFs and investments in single countries typically exhibit higher volatility. International, Emerging

Market and Frontier Market ETFs, mutual funds and individual securities may involve risk of capital loss from unfavorable

fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political

instability that other nations experience. Individual bonds, bond mutual funds and bond ETFs will typically decrease in

value as interest rates rise. A portion of a municipal bond fund's income may be subject to federal or state income taxes or

the alternative minimum tax. Capital gains (short and long-term), if any, are subject to capital gains tax.

Diversification and asset allocation may not protect against market risk or investment losses. At WT Wealth Management, we

strongly suggest having a personal financial plan in place before making any investment decisions including understanding

personal risk tolerance, having clearly outlined investment objectives and a clearly defined investment time horizon.

WT Wealth Management may only transact business in those states in which it is registered, or qualifies for an exemption

or exclusion from registration requirements. Individualized responses to persons that involve either the effecting of

transactions in securities, or the rendering of personalized investment advice for compensation, will not be made without

registration or exemption. WT Wealth Management's website is limited to the dissemination of general information

pertaining to its advisory services, together with access to additional investment-related information, publications, and

links.

Accordingly, the publication of WT Wealth Management's website should not be construed by any consumer and/or

prospective client as WT Wealth Management's solicitation to effect, or attempt to effect transactions in securities, or the

rendering of personalized investment advice for compensation, over the internet. Any subsequent, direct communication

by WT Wealth Management with a prospective client shall be conducted by a representative that is either regis

A copy of WT Wealth Management's current written disclosure statement discussing WT Wealth Management's registrations,

business operations, services, and fees is available at the SEC's investment adviser public information website (www.

adviserinfo.sec.gov) or from WT Wealth Management directly.

WT Wealth Management does not make any representations or warranties as to the accuracy, timeliness, suitability,

completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to WT Wealth

Management's web site or incorporated therein, and takes no responsibility therefor. All such information is provided solely

for convenience purposes and all users thereof should be guided accordingly.