Trade. How does the world define that term? Wikipedia's page says, "trade involves the transfer of goods or

services from one person or entity to another, often in exchange for money. A system or network that allows

trade is called a market."

Art. How would you define this term? Again, the world according to Wikipedia says, "Art is a diverse range

of human activities... expressing the author's imaginative, conceptual ideas, or technical skill, intended to be

appreciated for their beauty, emotional power, [discipline or effectiveness]."

We might then describe "The Art of the Trade" as a technical skill that results in the exchange (buy or sell) of

a security in such a way that a client can appreciate its "beauty" or "power" (i.e., contributing effectively to an

overall portfolio).

Introduction

AT WT Wealth Management, we have always strived to offer varied investment models in order to meet the

needs of every investor, large or small - ranging from ultra-conservative to ultra-aggressive.

Our current investment models include:

- A globally diversified allocation across a broad spectrum of regions and asset classes, in a rules-based

quantitative strategy available in a variety of risk tolerances (the "Quantitative" models),

- That same diversified and rules-based quantitative suite described above, with the additional feature

that the equity allocation is constructed with "smart beta" ETFs that seek to maximize risk-adjusted

returns (the "Quantitative Plus" models), and

- A variety of highly personalized, Separately Management Account ("SMA") strategies for higher-net-worth investors that blend Core holdings with Sectors & Themes and Culturally Significant Equities

(the "3-Pronged" models).

Over the course of the next year, we plan to produce a series of white papers focused on educating you about

our investment models and the philosophies and trading strategies behind them - the Art of the Trade series.

The information contained in this first paper focuses on the trading techniques employed to harvest and

realize gains that are used in the 3-Pronged models.

Overview

To begin on a personal note, one of the many things I love about my job is reviewing portfolios of new clients

when they join the firm. Sometimes I'm examining a self-directed account where the client had been making

their own buy and sell decisions, but decided to turn that responsibility over to an advisor. Other times, a new

client is leaving their previous advisor and I'm examining the buy and sell decisions of another advisor. In either

case it's always interesting to see how an account is allocated, the specific positions owned and the results of

those trade decisions.

In self-directed accounts I frequently ask the client questions about his/her overall strategy; why they own

certain positions; if they are "married" to any of them. The answers can range from "I don't really know" to

"I heard about it from a friend or family member" or "I saw it discussed on CNBC". None of those are really

wrong.

What I find could be improved in many clients' overall strategy (whether self-directed or professionally

advised) is the plan for how to make a profit on a position and what the expectations were when the trade

was initially made. Was it to own it forever? Was it to double their money? Was it to make 20% and walk away?

This is the art of the trade.

The Reality of Pressing Buy

Every trade should have a pre-planned exit strategy before you hit the buy button. This accomplishes two

things:

- It sets expectations about the anticipated results of the trade.

- It keeps you disciplined - fear and greed are powerful emotions.

Investing is intellectually and emotionally hard. It's very difficult to sell all or part of a position that has doubled

from $25 to $50. The natural thought process is to say, "I'm pretty smart! $100 can't be far off." On the other

hand, it's equally hard to buy more of a stock that you bought at $25 and is now at $15. The natural thought

process then is to say, "I'm a fool! How could I have made such a mistake?" Yet these counterintuitive, and

difficult, choices are often the very ones that should be made.

Blackjack

Many aspects of disciplined investing, or disciplined trading, can be very similar to disciplined gambling. The

inexperienced gambler might walk up to a blackjack table thinking, "if I don't lose too badly this might be fun."

Or, "if I can make enough for dinner I'll be super happy." Most sit down without any plan or exit strategy at all.

The casino loves these gamblers.

In blackjack, you might start with $300 and an hour later have $500. You're feeling great, sipping a cocktail

and making friends with everyone at the table. Forty-five minutes later, you leave the table with just $100, the

euphoria is gone and you mumble under your breath, "why didn't I quit when I was up $200 or at least quit

when I was only down $50?" "Why didn't I set aside $100 of my winnings for dinner?" The reason? No plan. . .

In fact, never even contemplated a plan -- after all, this was supposed to be just "fun".

Fade Trading

Trading or investing in equities can be very similar. Selling a winner is the only way to "realize" a gain. If you are

fortunate enough to buy a stock at $25 and have it go to $100, that $75 per share gain is unrealized. It's much

like the equity in your home. It really isn't yours . . . it's just a paper gain . . . until you make a decision to sell and

realize that increase. While a "trade" can be very hard to do in your home, it's incredibly easy in a stock. So a

savvy investor will consider harvesting gains as the stock appreciates. The proceeds from these realized gains

then are available as dry powder to pursue other opportunities, or simply as cash or income.

In SMAs, we generally allocate no more than 2%-4% to any individual equity. The allocation size is based on

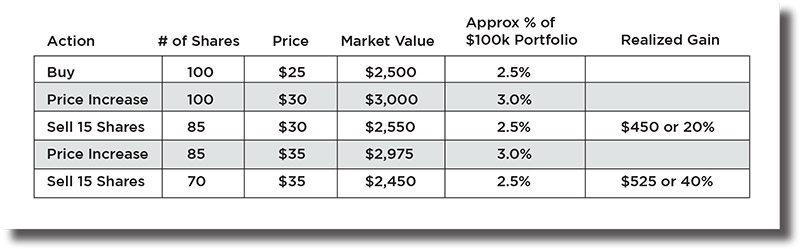

account size, investment objectives and tolerance for risk. Say we buy 100 shares of XYZ at $25 - that's $2,500,

or 2.5%, of a $100,000 portfolio. When XYZ gets to $30 per share we sell 15 shares and bring the position back

to its original allocation. Now let's say XYZ goes to $35. We sell another 15 shares to bring the position and

the weighting back down to the original allocation again.

Now, I know, clients will say, why sell 15 shares? What does that do? Well it locks in a realized gain of 20% (or

$450) on the first 15 shares sold and 40% (or another $525) on the second 15 shares sold. We like 20% or 40%

realized gains. We've also controlled the risk that the paper gains might disappear if the stock value declines.

This practice is what we mean by the term "fade trading". Maybe the stock loses some steam and gets back

down to $27 or $25 or even $23. Stocks do go up and down as you know. But we still have realized profit in

the position, because of the fade trading.

How does fade trading relate to blackjack? The same "fading or realizing of gains" strategy should be employed

when in the casino. Let's again say you start with $300 and when/if you get to $400 this time you stick $50

in your pocket and let the other $50 ride on your stack. Maybe you get lucky enough to get up another $100.

Same thing. . . $50 goes in your pocket and the other $50 remains on your stack. Here is the key. When your

money in play gets to $250 (i.e., $50 less than where you started at $300), you are done. The money in your

pocket is never part of the decision making process. You get up, thank the dealer and walk away with $100

in your pocket and $250 from the table for a total of $350. Since you started with $300, you've made a 17%

return.

When You Are Losing

Now let's look at how to handle losing situations - both when buying a stock or playing blackjack - because

those situations do happen. No one ever likes to buy a stock at $25 and then see it at $20 a month later. While

we like 20% gains, as above, 20% losses are no fun. At this point there are two things you can do: 1) Sell out or

2) buy more. Most of the time the professional investor, who still sees fundamental value in the stock, is going

to buy more - after all, a product you like is now "on sale". A professional investor will have done countless

hours of research into an individual stock position. Buying more of that position at $20 per share now should

be looked on as a great deal (when $25 was considered a great entry point just 30 days prior). As above, with

fade trading on the appreciating side, we now are going to maintain our initial 2%-4% weighting as the value

of the stock declines.

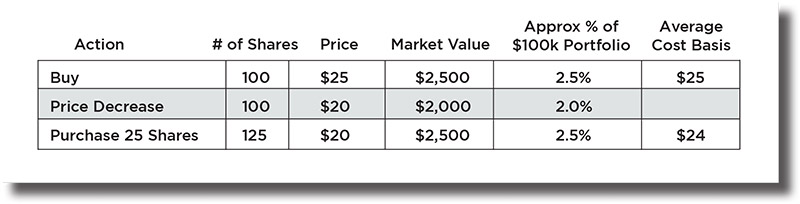

Using the example trade from above to illustrate, say we buy the same 100 shares of XYZ at $25 - that's

$2,500, or 2.5%, of a $100,000 portfolio. But in this case, XYZ falls to $20 per share. So we purchase 25 shares

and bring the position back to its original allocation.

This time we know clients will say, why purchase 25 more shares in a loser? What does that do? Well, it drives

our average cost basis on this position down from the original $25 per share to $24. And if our on-going

internal examinations solidify our belief that XYZ remains a buy, we have positioned the portfolio for greater

gains if a turnaround occurs. Through thick and thin, we continue with this disciplined approach until our

research, or our pre-established thresholds, tell us that we no longer like the stock.

Of course, sometimes research does actually tell us that we no longer like the stock. And sometimes a stock

does decline below the pre-established threshold. When either of those things occurs, it's time to make the

hard decision to exit a position and move on.

In blackjack, you shouldn't sit down at the table unless you know exactly how much you are willing to lose. Say

you start with $300 and are OK with a $100 loss. That's 20 $5 hands. (I've never seen anyone lose 20 straight

hands, but I bet it has happened). So if, after a period of time, you find yourself down the $100, you cash out

and walk away with your $100 loss. This does a few things. First, it hasn't thoroughly discouraged you from

ever gambling again. And second, it hasn't eviscerated your will to play blackjack in the future. You can revisit

the table to continue the fight later that day, the next day, or on a future visit.

Without an understanding that losses are part of investing and without understanding one's personal tolerance

to experience a loss, many clients reach a point where they simply want out after a market sell-off. "That's

it, I'm out and I'll never do that again!" I recently sat with one prospective client who liquidated his account

in 2010 and just could never bring himself to decide when was the next time to re-enter the market. He was

magical in talking himself out of pressing buy. That was 9 years ago and the client has sat on the sidelines

while the S&P 500 tripled in value!

WT Wealth Management is an SEC registered investment adviser, with in excess of $100 million in assets under management

(AUM) with offices in Flagstaff, Scottsdale, Sedona and Tucson, AZ along with Jackson Hole, WY and Las Vegas, NV.

WT Wealth Management is a manager of Separately Managed Accounts (SMAs). With SMAs, performance can vary widely

from investor to investor as each portfolio is individually constructed and managed. Asset allocation weightings are

determined based on a wide array of economic and market conditions the day the funds are invested. In an SMA, each

investor may own individual Exchange Traded Funds (ETFs), individual equities or mutual funds. As the manager we have

the freedom and flexibility to tailor the portfolio to address an individual investor's personal risk tolerance and investment

objectives - thus making the account "separate" and distinct from all others we manage.

An investment with WT Wealth Management is not insured or guaranteed by the Federal Deposit Insurance Corporation

(FDIC) or any other government agency.

Any opinions expressed are the opinions of WT Wealth Management and its associates only. Information offered is neither

an offer to buy or sell securities nor should it be interpreted as personal financial advice. Always seek out the advice of

a qualified investment professional before deciding to invest. Investing in stocks, bonds, mutual funds and ETFs carries

certain specific risks and part or all of an account's value can be lost.

In addition to the normal risks associated with investing, narrowly focused investments, investments in smaller companies,

sector and/or thematic ETFs and investments in single countries typically exhibit higher volatility. International, Emerging

Market and Frontier Market ETFs, mutual funds and individual securities may involve risk of capital loss from unfavorable

fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political

instability that other nations experience. Individual bonds, bond mutual funds and bond ETFs will typically decrease in

value as interest rates rise. A portion of a municipal bond fund's income may be subject to federal or state income taxes or

the alternative minimum tax. Capital gains (short and long-term), if any, are subject to capital gains tax.

Diversification and asset allocation may not protect against market risk or investment losses. At WT Wealth Management, we

strongly suggest having a personal financial plan in place before making any investment decisions including understanding

personal risk tolerance, having clearly outlined investment objectives and a clearly defined investment time horizon.

WT Wealth Management may only transact business in those states in which it is registered, or qualifies for an exemption

or exclusion from registration requirements. Individualized responses to persons that involve either the effecting of

transactions in securities, or the rendering of personalized investment advice for compensation, will not be made without

registration or exemption. WT Wealth Management's website is limited to the dissemination of general information

pertaining to its advisory services, together with access to additional investment-related information, publications, and

links.

Accordingly, the publication of WT Wealth Management's website should not be construed by any consumer and/or

prospective client as WT Wealth Management's solicitation to effect, or attempt to effect transactions in securities, or the

rendering of personalized investment advice for compensation, over the internet. Any subsequent, direct communication

by WT Wealth Management with a prospective client shall be conducted by a representative that is either registered or

qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

A copy of WT Wealth Management's current written disclosure statement discussing WT Wealth Management's registrations,

business operations, services, and fees is available at the SEC's investment adviser public information website (www.

adviserinfo.sec.gov) or from WT Wealth Management directly.

WT Wealth Management does not make any representations or warranties as to the accuracy, timeliness, suitability,

completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to WT Wealth

Management's web site or incorporated therein, and takes no responsibility therefor. All such information is provided solely

for convenience purposes and all users thereof should be guided accordingly.