A recent survey found that fewer than one in ten adults know the factors that determine their maximum social security benefit. Fortunately, the same survey also identified that more than nine in ten adults are eager to learn more about social security.

(1)

In this month's white paper WT Wealth Management felt an overview was appropriate. In other words, this is your opportunity to learn a little more.

The Basics

Social security is the major source of income for most of the retired and elderly.

(2)

- Nearly nine out of ten individuals aged 65 and older receive social security benefits.

- Social security benefits represent only about 33% of the income of the elderly.

- Among elderly social security beneficiaries, 50% of married couples and 70% of unmarried persons receive 50% or more of their income from social security.

- Among elderly social security beneficiaries, 21% of married couples and about 45% of unmarried persons rely on social security for 90% or more of their income.

Regardless of generation (Boomer+, Gen X, Millennial), roughly 60% of those who are not yet retired are worried they aren't saving enough for retirement and most believe they will need more income in retirement than what they expect to be provided by social security.

(1)

And they are right to believe that. Social security was never intended to be a retirement plan on its own. It was designed to be a supplement. Relying on social security without independent savings can be extremely risky. Generally, clients will need about 70% of their pre-retirement earnings to maintain their pre-retirement standard of living. With average earnings, social security retirement benefits will replace only about 40%.

(3)

Social security is a complex, and at times confusing, program. Since it can be the primary, or even sole, source of income for many retirees, a poorly informed decision can potentially have significant unintended consequences. As we sit with our pre-retiree clients, we found many just did not sufficiently understand the primary role that social security will play as a source of income during retirement or how to maximize benefits.

There are three key factors that should be discussed and reviewed when faced with decisions about social security benefits: timing, working in retirement, and taxes.

Timing

One-third of American workers claim social security benefits at 62. This is not full retirement age, but the earliest age at which they become eligible. By doing so, they lock in a lower-than-expected benefit for the remainder of their lives.

(3)

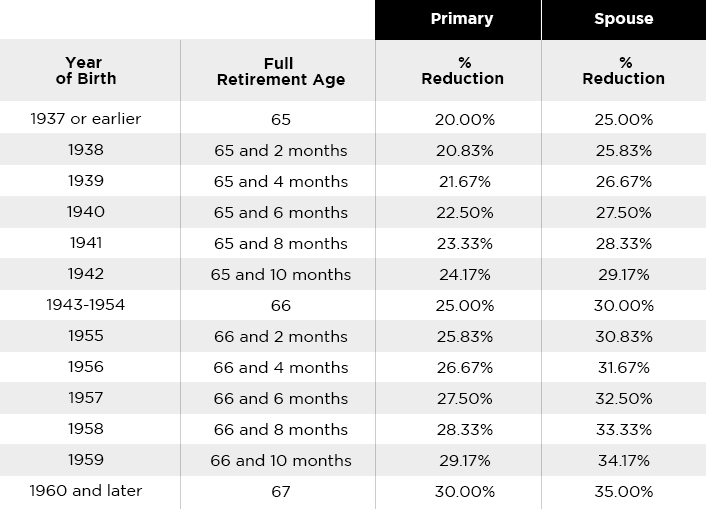

The Social Security Administration has prepared a table showing the impact of claiming early social security benefits at 62.

(4)

Primary and spousal benefits at age 62

It is important to remember that these reductions are not "corrected” once you reach full retirement age. They are permanent reductions that impact your social security benefits all the way through retirement.

So, if you don't desperately need the benefit at 62 when you first become eligible, it's financially wiser to wait. The benefits are even greater if you can wait until 70.

(5)

Working in Retirement

It is becoming more and more common for people to work and earn income during retirement – some by choice and others by necessity.

But earning too much can be costly if you are claiming social security benefits early. With the social security earnings test, as it is commonly known, you forfeit one dollar in social security benefits for every two dollars you earn over the income limit – which is $18,960 in 2021.

(6)

Happily, the social security earnings test disappears after you reach the full retirement age. So if you claimed social security benefits early, the excess taxation will end once you reach full retirement age. And if you wait until the full retirement age to begin taking social security income in the first place, additional income from continuing to work will have no impact on your social security benefits.

Taxes

If you receive income in retirement from sources other than social security, you may have to pay taxes on a portion of your social security benefit. For example, if a married couple file jointly, and their combined income is $44,000 or above, up to 85% of their social security benefits could be taxed.

(7)

Taxation is not determined by a person's age, but by income level and the corresponding tax bracket. While someone's tax bracket cannot be changed or appealed, there are ways to reduce or manage taxable income levels and thereby reduce effective tax rates.

At WT Wealth Management, we believe every client that is pulling retirement income from a variety of sources (e.g., IRAs, 401(k)s, annuities, pensions, social security, or simply continuing to work) should be working with a tax professional to identify every opportunity to reduce taxable income and minimize tax burden wherever possible.

Start Social Security Conversations Now

Because each person's circumstances are unique, there is no one-size-fits-all answer on when to begin taking social security benefits. But understanding how social security benefits are calculated can help you make the most informed decision.

Somewhere between just 30% to 40% of Americans work with a financial advisor. However, not all of those advisors are providing advice specific to social security benefits.

(1) So most Americans are left to figure out the complexities of social security on their own, making them vulnerable to making mistakes.

If you are approaching retirement age and have not discussed a social security strategy with your financial advisor, it is not too late! WT Wealth Management has access to industry leading social security analysis software that, combined with your advisor's extensive knowledge and experience and the guidance from tax experts at WT Tax Accounting, can help you make the best possible decisions for you and your family regarding your social security benefits.

Please reach out to your advisor if you would like to discuss more about retirement planning and the role of social security as you prepare for your golden years.

SOURCES:

- The Nationwide Retirement Institute® Social Security Consumer Survey

NationwideFinancial.com

- Fact Sheet - SOCIAL SECURITY

SSA.gov

- Complexities of Social Security

HartfordFunds.com

- Benefit Reduction for Early Retirement

SSA.gov

- Workers With Maximum-Taxable Earnings

SSA.gov

- Social Security Basics

Kiplinger.com

- Taxes on Social Security Benefits

Nolo.com