Are we in a recession? The long-accepted definition of two-consecutive quarters of negative GDP growth (-1.6% in Q1 2022 and -0.9% in Q2 2022) has been much debated of late. The strength of the employment market and enthusiastic consumer spending in the midst of declining GDP and high inflation has delayed formal acceptance of whether or not we truly are in a recession. While the debate rages, we thought we would look ahead at what an economic recovery might look like.

(1)

V-Shaped Recovery

V-shaped recessions don't last as long as other recessions, even after a steep drop. V-shapes tend to have the smallest long-term impact on overall GDP growth. Growth bounces back to previous trends after the recession, which is usually caused by a short-term interruption.

In a V-shaped recession, the economy has a steep dip but quickly recovers to its original path.

The sudden economic slow-down after the start of the Covid pandemic, in March 2020, is a good example of a V-shaped recovery. After a -3.5% Q1 2020 decline followed by a deep-pandemic driven -31.2% GDP decline in Q2 GDP, Q3 2020 GDP rebounded by 33.8% and GDP remained strong for the subsequent 3 quarters (4.5% in Q4 2020, 6.3% in Q1 2021 & 6.7% in Q2 2021).

U-Shaped Recovery

A U-shaped recession bounces back to its original growth path but only after a longer period of decline and/or stagnation than that caused by a prolonged period of economic decline. The trough of the GDP curve stretches out longer than in a V-shaped recession before eventually climbing back to the original growth expectations.

a U-shaped recession is similar to a V but with a longer recovery period that can take serveral years.

The last U-shaped recovery in the US economy happened between 1990-1991. This post-Gulf War recession was mild relative to other post-war recessions, but was characterized by a "jobless recovery," as unemployment continued to rise through June 1992 even though a positive economic growth rate had returned by late in the previous year.

W-Shaped Recovery

A recession that has a second dip after a recovery begins is a W-shaped recession. These can have a larger impact on consumer confidence because the second drop causes many consumers to hesitate longer than they otherwise might have before starting to spend money again, for fear of yet another dip in the future. W-shaped recessions don't always look like two Vs, maybe a V and a U.

A W-shaped recession has a second dip soon after the first. These recoveries can take many shapes. This graph shows a V followed by a U.

What is often referred to as the "Volker Recession" during the early 1980s was a W-shaped recovery. The Federal Reserve, chaired by Paul A. Volker, wrung inflation out of the economy but at a great cost — hurling the nation into two rapid succession recessions (Jan-Jul 1980 & Jul-Nov 1982) in an effort to kill inflation once and for all.

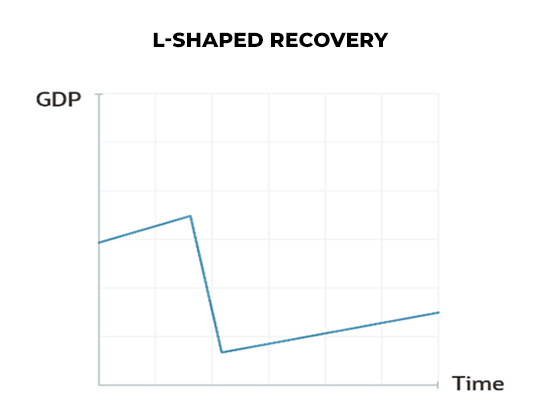

L-Shaped Recovery

L-shaped recessions can be the most worrying. They have long-term impacts on growth, permanently lowering GDP's growth trajectory and often approaching depression levels. Economic recovery is slow, unemployment remains high and investments stay low.

An L-shaped recession has a long recovery period; the economy generally does not return to its original growth path.

The post-2008 recession is a clear, recent example of an L-shaped recession, as GDP growth consistently stayed around 2% for many years afterward.

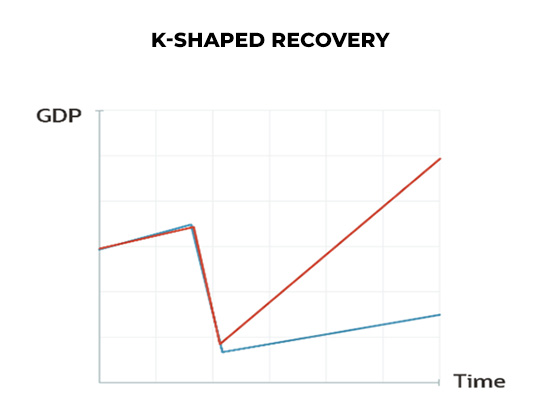

K-Shaped Recovery

Finally, a K-shaped recession reveals different recovery experiences in different parts of the economy. One group of consumers may experience a V- or U-shaped recovery, while the other group may experience more of an L-shaped recovery. The groups can be separated along industry, wealth, class, generational or demographic lines.

Typically, the recovery doesn't create these dividing lines, but reveals and enhances already existing economic differences among the groups.

In a K-shaped recession, different segments of the economy experience different rates of recovery. The red line shows an industry experiencing a V, where the blue line shows an industry experiencing an L shaped recovery.

The expanding wealth divide over the last few years points to a likely K-shaped recovery immediately ahead of us, in which low-income and high-income households will travel a vastly different road.

A Tale of Two Economies

As fears of a recession heat up, the economic situation for Americans seems to be going one of two ways.

One segment of America is racking up credit card debt, searching out cheaper brands, and picking up extra work, such as driving for Uber, DoorDash or pet sitting via Rover. According to a survey by Insuranks, some 44% of Americans are working at least one extra job and 28% have taken on a secondary gig to make ends meet each month. Inflation continues to gnaw away at household budgets, making it challenging to pay for basic expenditures like rent, food and gas.

(2)

Early pandemic-era policies provided a brief reprieve. Expanded unemployment benefits, three rounds of stimulus checks, and an eviction ban helped some lower-wage workers get ahead.

But in June this year, 64% of Americans were once again living paycheck to paycheck, per a LendingClub report, — a number that's ticked up in recent months as average savings have fallen.

(3) While most borrowers remain well-positioned to make payments, this is becoming much more challenging for lower-income households than those making more than $50,000 annually, per data from the New York Fed.

(4)

Adding to the problem is that workers' wages, while on the rise, haven't kept up with soaring inflation over the last several months to levels not seen in four decades. The result has been a decline in real wages. In June, the Labor Department said real average hourly earnings decreased 3.6% over the last 12 months.

Meanwhile, wealthier Americans seem to be doing just fine. While inflation is a nuisance, many have enough savings built up to continue spending. Given that the unemployment rate remains low, most can rely on a steady source of income and job opportunities even if they were to be laid off.

Inflation is the Differentiator

Inflation is a tax on all of us and has been the boogeyman since the early 1980's because it's so destructive. No one is above it or successfully avoids it. If you buy gas, consume food and stock your home with soft goods you are paying at least 10% more and in some cases 20% or 30% more. Inflation is particularly destructive to lower- and middle-class Americans, who were already stretched thin.

In a breath of fresh air, the Bureau of Labor Statistics' latest Consumer Price Index (CPI) report on August 10th showed inflation eased slightly, reflecting a year-over-year increase of 8.5% in July (down from June's 40-year high of 9.1%). A downward trend in gasoline prices over more than 50 consecutive days contributed to the relief. Still, inflationary pressures remained strong across other components of the report and declining gas and energy prices were offset by increases in the food and shelter indexes, the BLS report indicated.

(5)

It feels funny to celebrate 8.5% inflation, but at least we appear to be moving in the right direction.

Conclusion

At WT Wealth Management, we are closely watching the monthly Consumer Price Index (CPI) and Producer Price Index (PPI) reports. The "transitory" inflation ship has sailed. So we hope that the Federal Reserve’s actions over the last few months have started making a dent in the inflationary pressures every American is feeling.

Sources

- Types of Economic Recessions Explained

NetSuite.com

- Hidden reality of new jobs report

TheOhioStar.com

- As inflation heats up, 64% of Americans are now living paycheck to paycheck

CNBC.com

- The US economy is splitting in 2

BusinessInsider.com

- Inflation moderates in July as CPI rises at less-than-expected 8.5%

Finance.Yahoo.com