At WT Wealth Management, we take pride in educating our clients on current news and events. We have long maintained that an educated investor is a better, more patient, and successful investor. Our hope is that the subjects we tackle in our White Papers and Special Market Updates are timely in addressing the events affecting your investments.

Nearly everything we read and hear about today revolves around the Fed Funds Rate (FFR), commonly referred to as "the interest rate." Changes in the Fed Funds Rate can trigger a chain of events that affect other short-term interest rates, foreign exchange rates, the availability and cost of credit for consumers, and, ultimately, a range of economic variables including employment and prices of goods and services (i.e., inflation).

The Federal Open Market Committee (FOMC) is responsible for open market operations and setting the overnight lending rate commonly referred to as the FFR. The FFR is the interest rate at which depository institutions lend balances at the Federal Reserve to other depository institutions overnight.

(1)

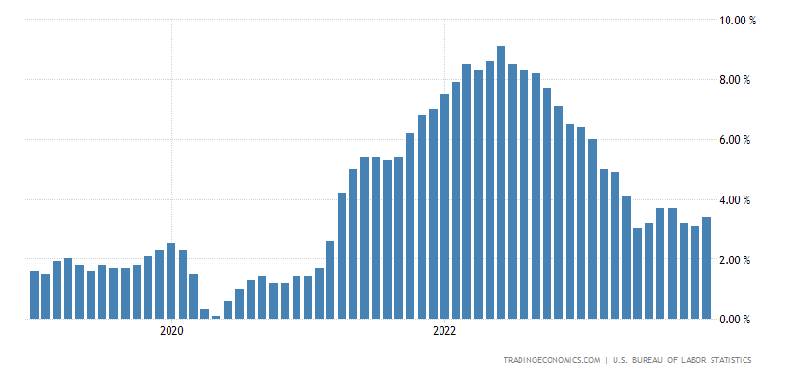

The million-dollar question is: has the FOMC done enough to combat inflation; can they now start to cut interest rates? There's an old saying that the Fed shows up late to the party and then overstays their welcome. There's little doubt that as inflation accelerated in late 2021/early 2022, the FOMC "showed up late to the party," and inflation (as defined by CPI - Consumer Price Index) surged to a multi-decade high, reaching a peak of 9.1% in June of 2022.

(2)

Should the Fed have raised rates sooner? In hindsight, almost certainly yes.

Figure 1: Annual % Change in the United States Consumer Price Index

Source: U.S. Bureau of Labor Statistics

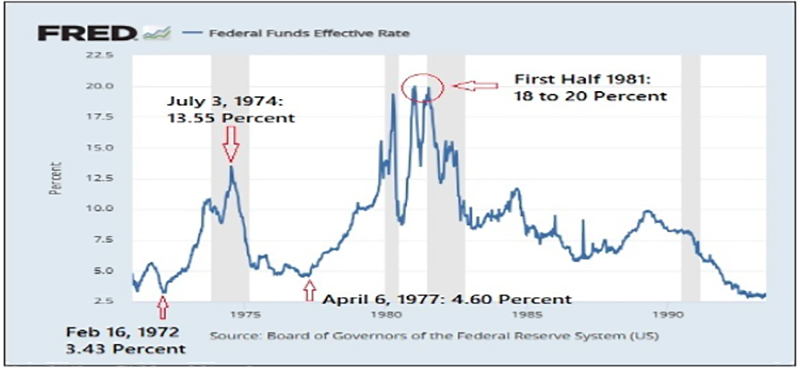

Today, the investment community closely watches the FOMC to see if they "overstay their welcome" and cause a recession as a result of interest rates being "too high for too long." It's a very delicate situation to achieve the inflation target but not push the US economy into a recession. The FOMC has vowed to defeat inflation and keep rates higher for longer to ensure inflation is thoroughly defeated. Back in the mid-late 1970s and early 1980s when then Fed Chair Paul Volcker thought he had inflation whipped, the Fed prematurely cut interest rates, and inflation returned. The chart below shows a 1974 high on the FFR of 13.55% and subsequent cuts into 1977 down to 4.60%. As a result, the Fed had to come back harder and higher, raising the FFR to a historic 20% in 1981, causing a double-dip recession.

(3)

Today's FOMC has pledged to learn from history and not cut rates prematurely. As a result, we have heard a constant mantra from the Fed over the last year of "higher for longer." The last rate hike was on July 26th, 2023, nearly 7 months ago. Does the Fed consider seven months "longer"? Or do we need 3, 6, or 9 more months of the current interest rate level to ensure inflation has been defeated? That is the question the Fed, economists, and Wall Street observers are trying to determine. The one thing we do know is that the longer rates are in a restrictive range, the greater the chance of the Fed "overstaying" their welcome and causing a recession.

We used the term "restrictive" in the previous paragraph. What does that mean? In the simplest terms, if the FFR is higher than the inflation rate, most economists consider that restrictive monetary policy. If the FFR is lower than the current inflation rate, it's considered accommodative, and if the FFR is near or at the current inflation rate, it's considered neutral. We currently have an FFR of 5.25-5.50% with an inflation rate, using the Fed's preferred gauge of Core-PCE, of 2.9%, or CPI of 3.4%; therefore, by that commonly accepted definition, the Fed is currently employing restrictive monetary policy.

Lower interest rates generally allow for greater economic expansion than higher rates. This should make sense as the cost of borrowing for a home, car, credit card, or for a small or large business wanting to expand is less expensive with lower interest rates. However, rates too low can lead to a reemergence of inflation, and that hurts everyone.

In our opinion, the economy has performed quite well over the last year despite 20-year highs in the FFR. Thankfully, unemployment remains under 4%, Gross Domestic Product (GDP) has been strong, and higher interest rates have slowed but not destroyed the housing market as many predicted. Back when the Fed started raising rates in March of 2022, not many would have predicted this good of an economic outcome if they knew the Fed would have to get the FFR above 5%. It had been since June of 2006 that the FFR had been that elevated.

(4)

The Investment Committee at WT Wealth Management believes the Fed has done an exceptional job despite being "late to the party". They have communicated in a clear and transparent way over the last year, and we feel they are well aware they can't overstay their welcome without a disastrous outcome, which they'll be even more aware of in an election year.

However, we do see a continued "higher for longer" period than many Wall Street fortune tellers who see cuts in March and/or June, and we feel the first rate cut will not happen until early-to-mid-summer provided inflation continues its slow decline toward the Fed's 2% target. If cuts occur sooner, great, but we would not dictate investing strategies based on "early or imminent" rate cuts.

Firming our monetary policy beliefs was the FOMC statement on January 31st, after the 2-day FOMC meeting where Fed policymakers gave no immediate indication as to when rate cuts would occur nor to what degree. In fact, they reiterated that it would not be appropriate to change the FFR until they were confident of a continued decline to the 2% inflation goal. So, we maintain our "higher for longer" FFR view but believe there is enough slowing at the margins to get several rate cuts by the end of the year (June, September, and December would be every other FOMC meeting and seems plausible).

We hope this clarifies much of the Federal Reserve monetary policy jargon that is often thrown around, and we have translated the basics of monetary policy in an easy-to-understand approach. As always, please reach out to your financial advisor with any questions to ensure your portfolio is aligned with your goals, objectives, and overall risk tolerance.

Sources

- Federal Open Market Committee

federalreserve.gov

- Here's the inflation breakdown for September 2023 - in one chart

cnbc.com

- These Charts Show Why the Fed Is Terrified to Stop Raising Interest Rates and Why Nasdaq Is Ripping Higher

wallstreetonparade.com

- Federal Funds Target Rate History

fedprimerate.com